Proficient Auto Logistics 🇺🇸

NASDAQ: PAL • EV: $255M • Last Close: $7.05

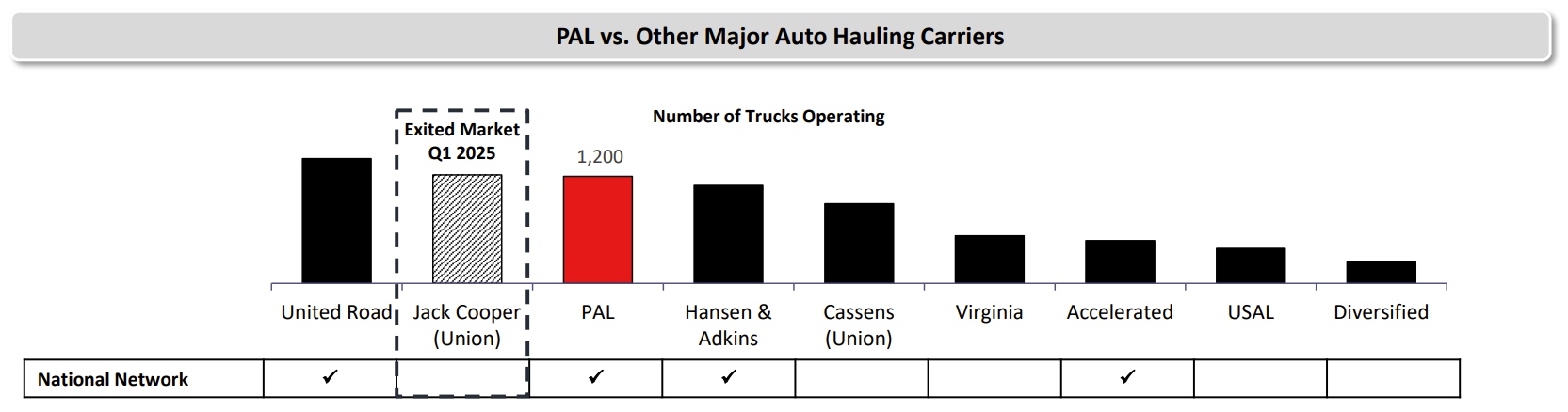

Proficient Auto Logistics is a LTL freight transportation company focused on auto-hauling. They transport new cars from auto OEM’s to dealerships. The auto-hauling LTL market recovery has lagged the broader LTL recovery. This looks like it will soon change due to the bankruptcy of competitor Jack Cooper and other smaller players.

Today they’re trading for an EV/EBITDA of ~7.5x. On more normalized/mid-cycle numbers this would be 5.5x. LTL peers trade for around 12x to 18x.

A Great Writeup from Everyone Hates Poetry (Link).

A Writeup from Everyone Henrik Alex (Link).

Tab Gida 🇺🇸

IST: TABGD • EV: USD $1.2B • Last Close: ₺233.40

Tab Gida is the master franchisee for Burger King and Popeye’s in Turkey. They are twice the size of the nearest QSR competitor and control their own processing facilities, bakeries, and logistics.

“[The Kurdoğlu family] bring an engineering-minded mindset to fast food. I have never seen any fast-food team anywhere in the world that is as good as theirs. These guys are better than any franchisees I have ever interacted with. They backward integrated heavily. They are detail-oriented on all the finer points. They are looking at all the nuances carefully. That is the reason why they made mincemeat of McDonald's.”

- Mohnish Pabrai

Shares trade for ~12x earnings with a long runway for continued expansion of both current and additional brands.

A Writeup from Lunch Investing (Link).

Ferrari Group 🇮🇹

AMS: FERGR • EV: USD $634M • Last Close: €7.95

Ferrari Group, different from Ferrari NV, is a family run luxury logistics company. They ensure that very high-end products like jewelry, diamonds and watches make it safely from companies warehouses to stores, between stores, and directly to customers. Ferrari’s services are integrated into customer operations through shared facilities and IT systems. Their security employees, armored vehicles, vaults, and procedures are all designed specifically for luxury items. Transport costs are very small compared to the value of customers products. It is not worth the risk of disappointing a client to save a tiny amount of money.

Ferrari has grown throughout the recent luxury downturn highlighting the durability of the business. Shares trade for an EV/FCF of 8x. They earn a 30% ROIC and management has targeted medium term 6% - 8% topline growth.

A Recent VIC Writeup (Link).

A Writeup from The Dutch Investors (Link).

Check Out: Same Process. Different Outcomes.

Disclosure: This newsletter does not provide investment advice. Information presented is for informational purposes only and should not be considered a recommendation to buy or sell securities. The author may or may not own the securities discussed.