Nintendo owns some of the most valuable IP in the world. This IP is fueling a business transition akin to the Apple/iOS playbook. Meanwhile, short-term oriented investors are missing the forest for the trees and have sold shares down to a laughable valuation.

From selling playing cards to the Yakuza to a newly hired art school graduate single-handedly saving the company with the overnight success that was Donkey Kong, Nintendo’s origins are interesting to say the least. For the full story, the two-part Nintendo series from the Acquired Podcast is a must listen.

I first got to know Nintendo via Crossroads Capital’s work. The below writeup draws heavily on their thinking and analysis. For further reading I highly recommend their 2018 and 2021 annual letters.

*Most of the charts and figures in this report are AI generated. The writing remains entirely my own. All figures are in USD unless otherwise noted.

The Ecosystem Blueprint

The success of Apple and their ubiquitous iOS ecosystem are well known. Investors have been rewarded handsomely with the stock returning 26% annually since the iPhones debut in 2007 (that’s an 80-bagger). While there are some important differences, the Nintendo of today looks very similar to the early days of the Apple iOS journey.

Over the past two decades Apple has created an incredibly sticky hardware-software ecosystem, one that ~90% of iPhone users choose to stick with when buying their next phone. The success of this ecosystem is largely attributable to the following key attributes:

1) Apple releases a new iPhone every year, each with its own models across different price points. New iPhones are launched with smaller incremental upgrades. They don’t have to worry that each new iPhone might be a total flop, because they’re all still basically the same device that millions of users love.

2) Apple maintains a virtually identical user interface across different device generations. Your 83-year-old mother or grandmother upgrading from an iPhone 12 is able to immediately start using today’s latest and greatest iPhone 17 with essentially no learning curve.

3) Apple ties users to its platform via user accounts and cloud-based data storage. Transferring apps, photos, message history, and contacts from old iPhones to new ones is seamless.

4) Last and most important, Apple maintains forward and backward compatibility. New iPhones run all existing iOS apps and older iPhones continue to run almost all new iOS apps. Developers know that all Apple iOS devices will continue to run their apps across generations. They also know Apple will continue to sell more and more iOS devices, growing the market for their apps over time. This dynamic means that the App Store has a far better selection and quality of apps than what is available on Android devices. This in turn makes Apple’s App Store more valuable to iPhone users. This self-reinforcing software-hardware iOS ecosystem is the key to Apple’s success and is what drives their ~$120B of high-margin App Store and services revenues.

“Apple’s iPhone is not simply a single purchase device, but a ticket into a one-of-a-kind indefinitely-lived software-based ecosystem.”

- Crossroads Capital’s 2021 Annual Letter

Nintendo: Past vs Present

The Hardware-Software Ecosystem

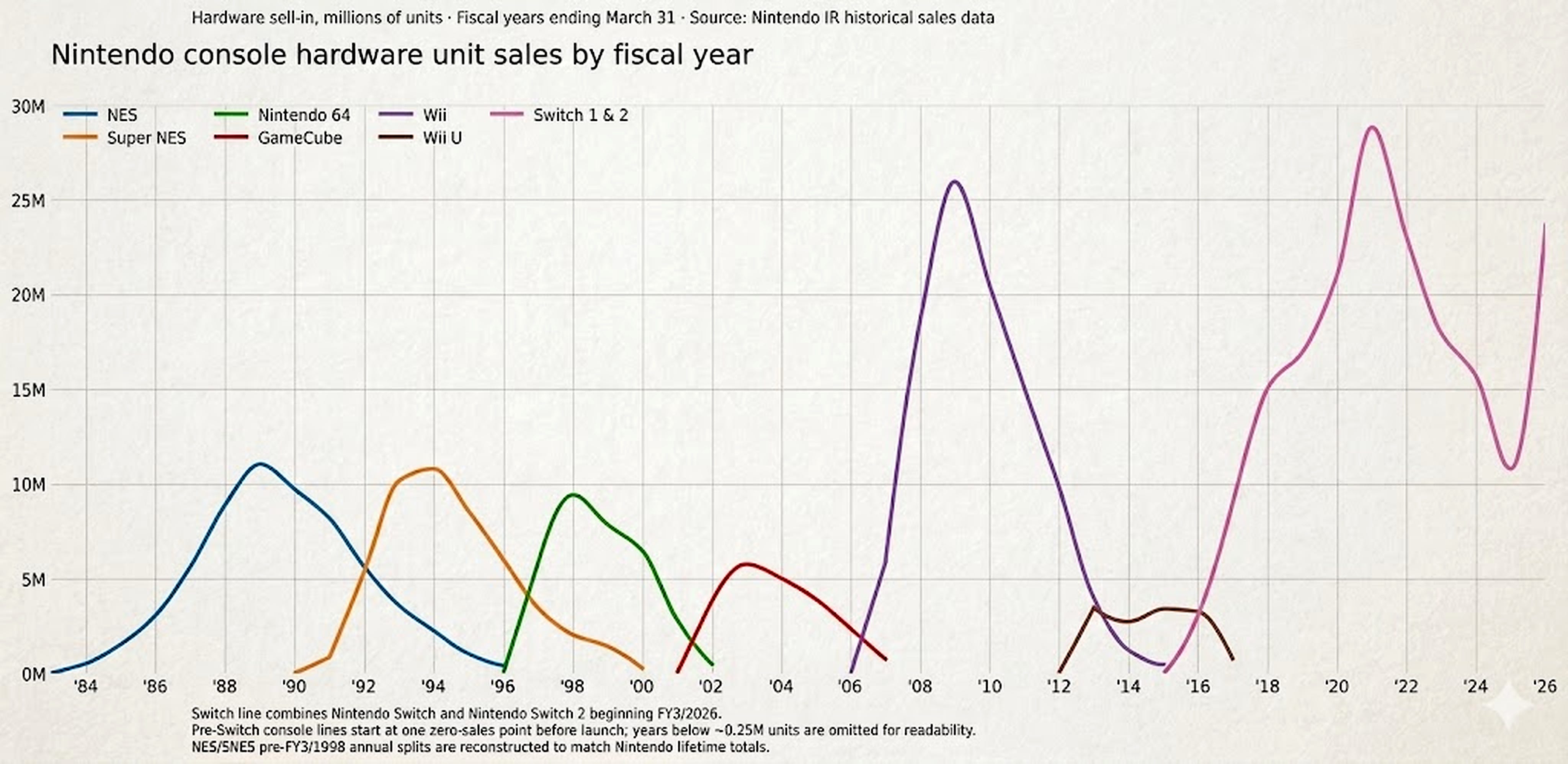

Prior to the Switch, Nintendo’s business model was one of feast or famine. After every console generation they needed to rebuild their user base from scratch. This meant huge swings in profitability as they went from hit success to flop (Wii to Wii U).

A successful console needs lots of users. To get lots of users, you need lots of good games. The catch though, is that game developers only make games for consoles with lots of users. Without a certain critical mass of users to kickstart this network effect, a new console inevitably turns into a flop. This dynamic drove once-mighty companies like Atari and Sega out of the console business and is the reason why Nintendo has historically held such a large cash balance in reserve.

But what if rather than reinventing the wheel every console generation, you instead continuously improved an already successful one indefinitely? Well, Nintendo has hinted at doing this as early as 2014.

“Consoles and handheld devices will no longer be completely different, and they will become like brothers in a family of systems… To cite a specific case, Apple is able to release smart devices with various form factors one after another because there is one way of programming adopted by all platforms. Another example is Android. Though there are various models, Android does not face software shortages because there is one common way of programming on the Android platform that works with various models. The point is, Nintendo platforms should be like those two examples.”

- Satoru Iwata, Former Nintendo President/CEO, 2014 Investor Call

And again more explicitly during a 2018 investor presentation:

“Up until now, the hardware lifecycle has trended at around five or six years, but it would be very interesting if we could prolong that life cycle, and I think you should be looking forward to that.”

- Shigeru Miyamoto, Nintendo Creative Lead

By transitioning to an iterative rather than one-off hardware model, Nintendo is creating a user base that continuously grows and never resets. As the iPhone has proven, one of the keys to success here is forward and backward compatibility. With the Switch 2, Nintendo has now implemented this all important feature. New devices run already existing games while old devices maintain forward compatibility to run most new games.

Nintendo has also launched Nintendo Switch Online (NSO), their subscription-based online gaming service which gives users free content, exclusive offers, and access to vintage games. More importantly, for the first time in company history, users can now easily transfer games, services, and data across devices.

“Nintendo’s relationship with customers is no longer based on a hardware device, but on their Nintendo Account that persists across multiple devices and which can now be continuously monetized.”

- Crossroads Capital’s 2021 Annual Letter

Just like Apple’s iPhone family of devices, the Nintendo Switch family of devices is now “forever”. The market does not fully appreciate this.

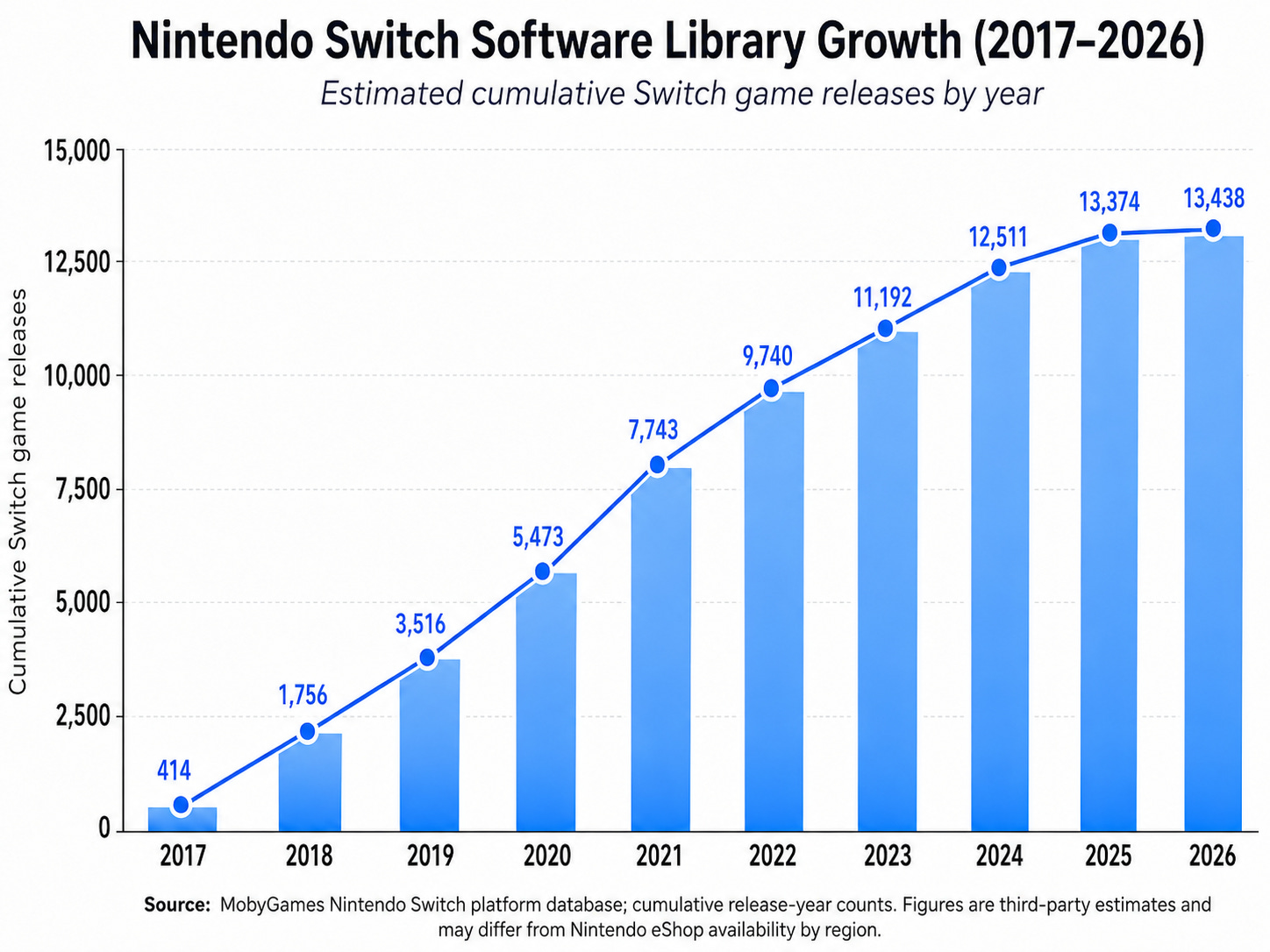

As mentioned already, lots of good games sells lots of consoles. The Switch’s indefinitely-lived hardware-software ecosystem means Nintendo and third-party developers can sell software titles, both new and old, into a massive and continuously growing installed base. The number of third-party software titles available on the eShop continues to grow and now represents over 50% of gross sales compared to ~30% in 2019.

Adding further momentum to the flywheel, the Switch, like the iPhone and unlike past Nintendo consoles, relies on off-the-shelf mobile components instead of custom ones. This lets Apple and now Nintendo ride the continuous mobile cost curve downward. Similar to how a flat screen TV that cost $2,000 in 2005 costs $200 today. The price of older Switch models will drop, boosting unit sales and expanding the Switch family’s user base.

Furthermore, today’s third-party game development engines like Unity make it much easier for game developers to make games for multiple platforms. The Switch is more friendly and more attractive to third-party developers than ever before.

Thanks to Nintendo’s transition to an indefinitely-lived Switch ecosystem, the eShop is quickly becoming an App Store-like third-party software distribution platform. One where software sales, not hardware sales drives earnings power.

The IP Flywheel

While Nintendo’s IP library has historically been under-monetized, this is quickly changing via a renewed push into theme parks, movies, and retail locations. While profitability is not the primary focus, Nintendo’s IP segment is nonetheless creating multiple high-margin, annuity-like revenue streams. More importantly, the real benefit of these new IP initiatives is reaching present and future Switch users.

Let’s take a look at the developing Nintendo Cinematic Universe. In 2023 Nintendo returned to the movie business for the first time in 30 years with The Super Mario Bros. Movie. A blockbuster that reached over 170M people in theatres and generated $1.4B in gross revenue at the global box office. Its sequel, The Super Mario Galaxy Movie, released this April has already grossed $1B. A live-action Legend of Zelda film is slated for 2027, after which management has confirmed it will “work up to a regular release schedule of one movie per year”.

These unique exposures to Nintendo’s IP reinforces the core Switch Platform business. The Super Mario Bros. Movie for example reached well over 400M viewers across theatres and streaming services. 6 months after the films release, Nintendo released a hugely successful new Mario game. Nintendo is now regularly gaining more exposure to potential customers than ever before in its history. Not only that, but they are doing so at a negative customer acquisition cost. Super Mario Bros earned an estimated $560M on a production budget of $100M! Reaching the same number of viewers via 30-second YouTube ads would cost up to $20M.

Nintendo is running the same playbook with theme parks. Super Nintendo World has proved a huge success for Universal who pays royalties to Nintendo, likely in the high single digit range of all park revenue.

Comcast has repeatedly cited Super Nintendo World as a contributor to growth at Universal’s theme parks.

“Domestic theme parks revenue increased, reflecting higher revenue at our theme park in Hollywood due to the continued success of Super Nintendo World, partially offset by lower revenue at our theme park in Orlando…”

- Comcast Q4 2023 Earnings Release

Nintendo’s IP is drawing more users into the Switch ecosystem, which encourages more games to be developed for the eShop, which in turn draws more users into the ecosystem, and so on.

The Pokémon Company

Nintendo owns stakes in a handful of various businesses, the most material of which by far is The Pokémon Company (TPC). While Nintendo’s reported stake in TPC is 33%, its real ownership is likely at least 50%.

TPC is owned one third each by Nintendo, GameFreak, and Creature Inc. What isn’t disclosed is Nintendo’s equity stakes in either Creature or GameFreak. Under Japanese securities law, Nintendo is not legally required to disclose its stakes in them. While not reported, Nintendo almost certainly owns material stakes in each. For example Game Freak already develops almost exclusively for the Switch and literally works out of offices on Nintendo’s corporate campus.

These undisclosed stakes are part of a classic Japanese cross-shareholding tactic aimed at obscuring Nintendo’s de facto control of TPC and makes uncovering the extent of Nintendo’s empire difficult by design. In past eras this made sense if you wanted to guarantee survival for the next 100 years. However with Japanese corporate culture slowly changing, this is no longer the case. Fully consolidating Nintendo’s full economic interest in TPC, as was done in 2021 with another of Nintendo’s partner studios, Next Level Games, remains a major future catalyst.

Also unmentioned in Nintendo’s filings is its ownership of the actual Pokémon trademark and the associated trademarks of individual Pokémon characters, which it licenses to TPC. TPC merely acts as its agent, overseeing the global licensing operations of the Pokémon business empire. With this in mind, ask yourself, who really owns The Pokémon Company? While impossible to narrow down, everything points to Nintendo’s true ownership of TPC landing at at least 50%. For further reading on the topic I’d recommend this article.

TPC is perhaps the most valuable media entertainment IP on Earth.

TPC’s latest reported annual revenue was $3.5B, which given the low-cost nature of collecting royalties should throw off annual FCF of approximately $2.6 billion. A high-margin, highly recurring media franchise such as Pokémon is worth 20x FCF any day of the week. Conservatively assuming Nintendo’s stake in TPC at 50% gets us to a value of $26B.

Other stakes include DeNA, Bandai Namco, Niantic Spatial, and 10% of the Seattle Mariners (yes, you read that correctly, Nintendo saved the team from moving to Tampa in the 90’s). Together, these are worth around $1B.

What is The Market Missing?

The IP fueled transition to an indefinitely-lived hardware-software ecosystem discussed above is a multi-year, if not multi-decade process. While Nintendo and long-term investors such as myself are focused on the health of the business over the long-term, the market at large is not.

“As the CEO and Manager of Nintendo, I should not be too concerned with very short-term share price fluctuations, otherwise we will lose sight of what’s really important.”

- Satoru Iwata, Former Nintendo President/CEO, 2004 Interview

“A year is actually less than the average product development cycle… development for most of them started two or three years ago… some software even have a timeline of 3 to 4 years because what we start making today needs 3 to 4 years before they can exhibit their real worth.”

- Satoru Iwata, Former Nintendo President/CEO, 2009 Investor Q&A.

“It is difficult to predict the changes in the external environment… but I think it is not an appropriate approach to be excessively influenced by short-term trends…”

- Shuntaro Furukawa, Nintendo President/CEO, 2026 Investor Q&A.

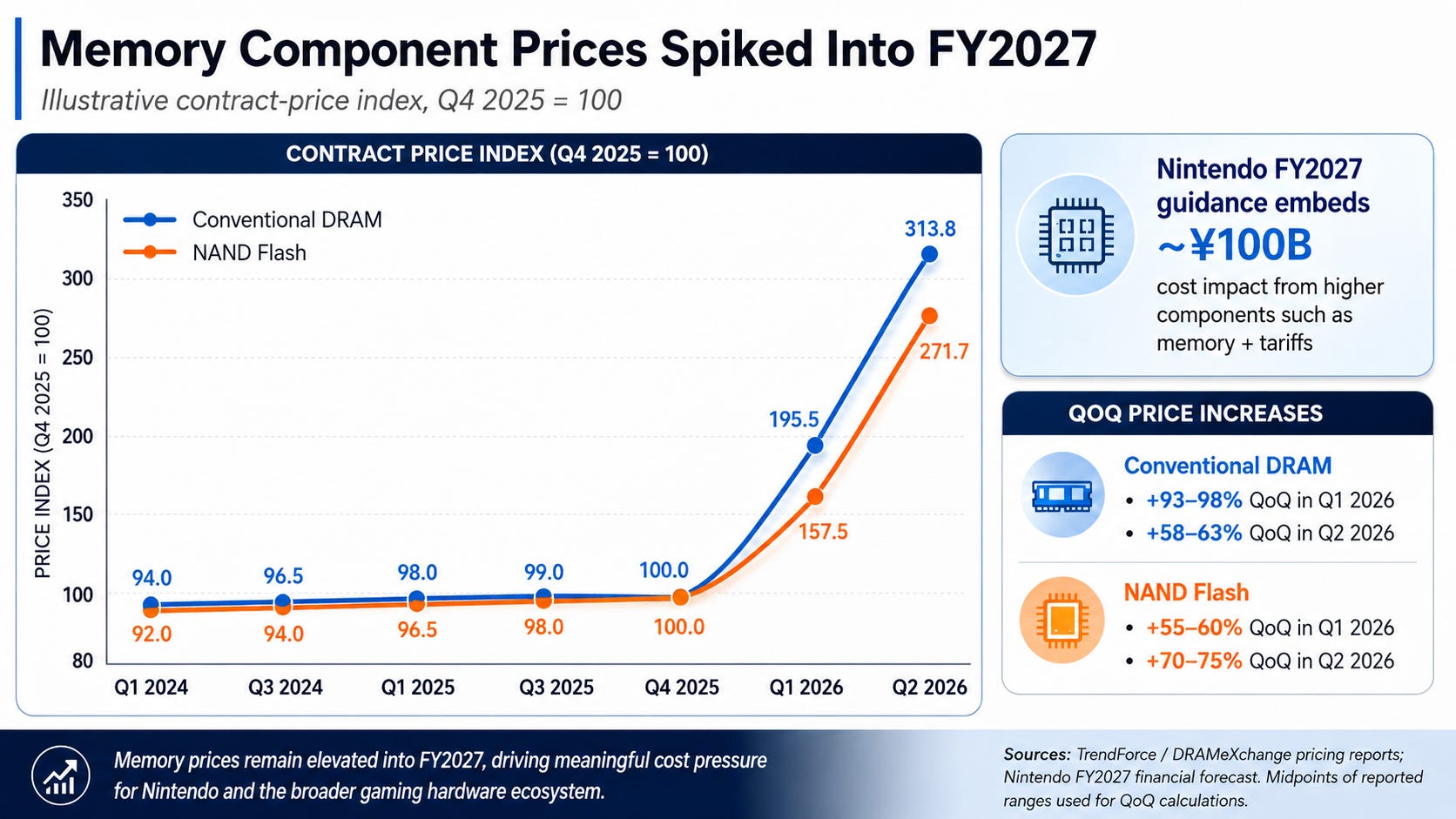

Investors are fixated on short-term headwinds that are not relevant to Nintendo’s long-term earnings power. These include 1) margin compression from memory card prices, and especially 2) weak FY27 guidance. These two factors when combined with the markets overemphasis on quarter-to-quarter results has shares down 50% from their 52-week high. This is a blessing in disguise as the market is missing the forest for the trees here. While investors panic over misplaced fears, we get a chance to purchase shares at their most attractive valuation in over 5 years.

Memory Card Margin Compression

As part of the AI compute demand bonanza, memory card prices have gone through the roof. Investors are concerned over input costs and the resulting pressure on Switch hardware margins.

Management expects a ~$600M FY27 earnings drag from memory/components and tariffs. The timing of this headwind with the launch of the Switch 2 is unfortunate and while the numbers are certainly not insignificant, the hardware margin pressure obscures the longer-term picture. Ultimately, it’s Nintendo’s software sales and third-party monetization that drives the earnings power of the business.

Nintendo announced Switch 2 price increases in May as a direct result of rising component costs. This takes us to what investors are primarily concerned about, go-forward Switch unit sales.

FY27 Guidance

The Switch 2 sold 19.8M units in FY26, its first year on the market. Expecting continued momentum, investors were disappointed with management’s FY27 guidance of only 16.5M units. The recent price hike from $449.99 to $499.99 has further raised fears over the declining Switch sales narrative. This narrative is wrong though, looking past the noise there is ample evidence suggesting the future ahead is bright for the Switch 2.

Nintendo is infamous for sandbagging guidance. They initially guided for only 15M Switch 2 units in FY26 despite selling almost 20M. Since FY2018 they’ve under-guided hardware units by an average of 10% and software units by almost 30%. The light FY27 guide should not be of concern and is simply a reflection of management’s overly conservative nature. According to a recent Bloomberg article, Nintendo has already asked partners and suppliers to assemble 20M Switch 2 units for FY27.

Unlike the original Switch which had a stacked first year of “system seller” game releases. Nintendo has strategically back-loaded its biggest Switch 2 games. The biggest driver of hardware sales is games, and Nintendo is positioning itself for sustained momentum across the Switch 2’s life cycle rather than risking a mid or late generation drought.

“…it is not an appropriate approach to be excessively influenced by short-term trends. The second and third years for Nintendo Switch 2 are very important, and if we can expand the hardware installed base, we can use that as a basis to greatly expand software sales.

- Shuntaro Furukawa, Nintendo President/CEO, 2026 Investor Q&A.

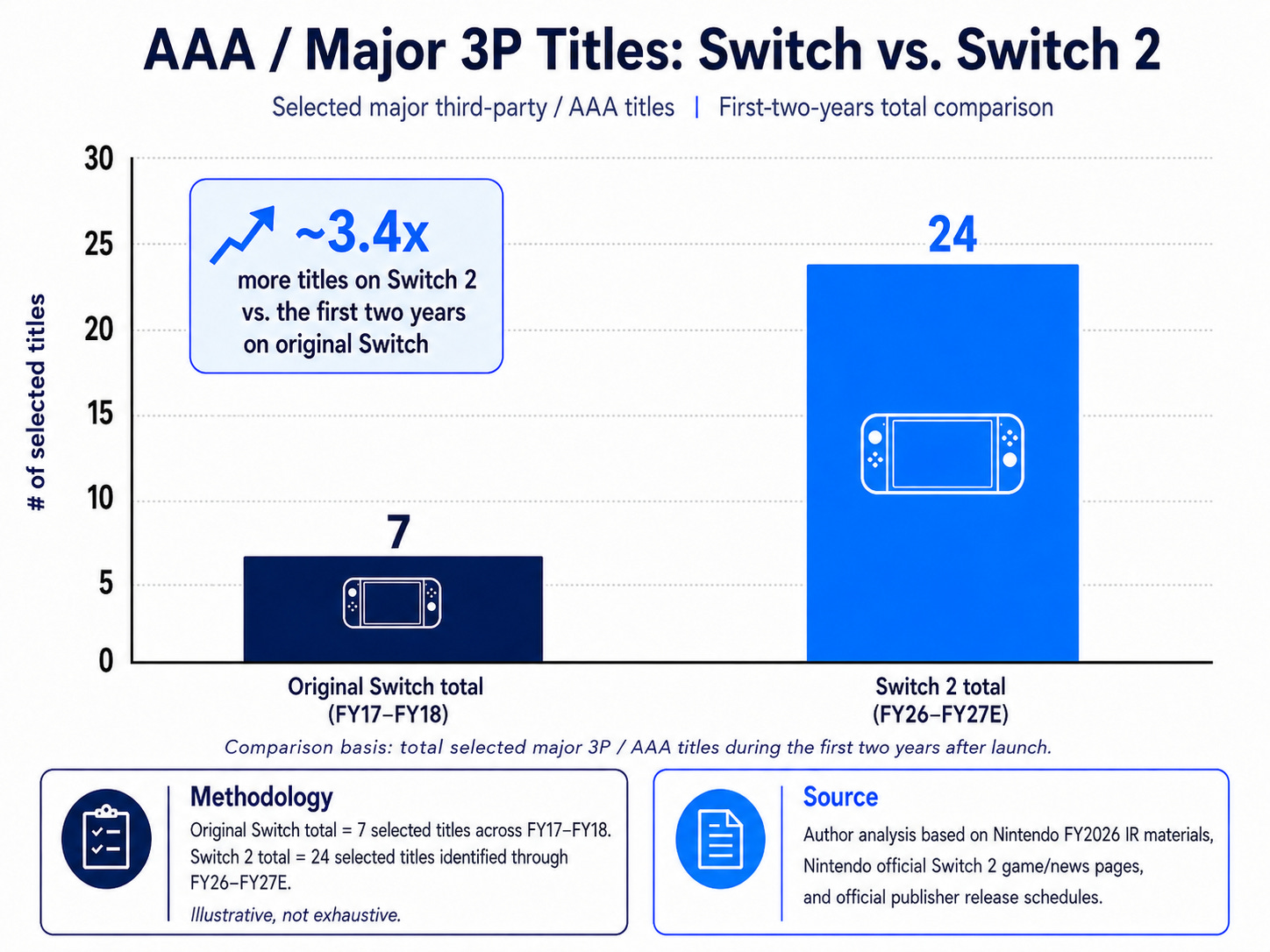

The Switch 1 benefited from an unusually strong launch year, including Super Mario Odyssey, Mario Kart 8 Deluxe, and Game of the Year winner: The Legend of Zelda: Breath of the Wild. The Switch 2 on the other hand launched with just one new system seller, Mario Kart World, which was later supplemented by Donkey Kong Bananza. Upcoming major Switch 2 releases include Splatoon Raiders, Pokémon Pokopia, and importantly, a rumored new 3D Mario and Legend of Zelda remake.

Upcoming first-party Nintendo system sellers aren’t the only thing to be excited about, the Switch 2 has also seen a step change in the availability of third-party AAA games. The Switch 2's more powerful hardware allows today's major multi-platform titles to run natively, without the technical compromises that accompanied the original Switch. While AAA games on the Switch were limited and with release dates well behind PS4/Xbox deputs, the Switch 2 already has an impressive AAA lineup including titles like Call of Duty and Cyberpunk 2077 with release dates matching PS5 and Xbox.

“For the first time in history, gamers are able to play high-powered AAA titles not just at home, but on the go with dedicated controls.”

- Crossroads Capital’s 2021 Annual Letter

Again, it’s critical to highlight that when it comes to video game consoles, software sells hardware, not the other way around. With this in mind, the Switch 2’s most important software releases are ahead of it, not behind it.

Valuation

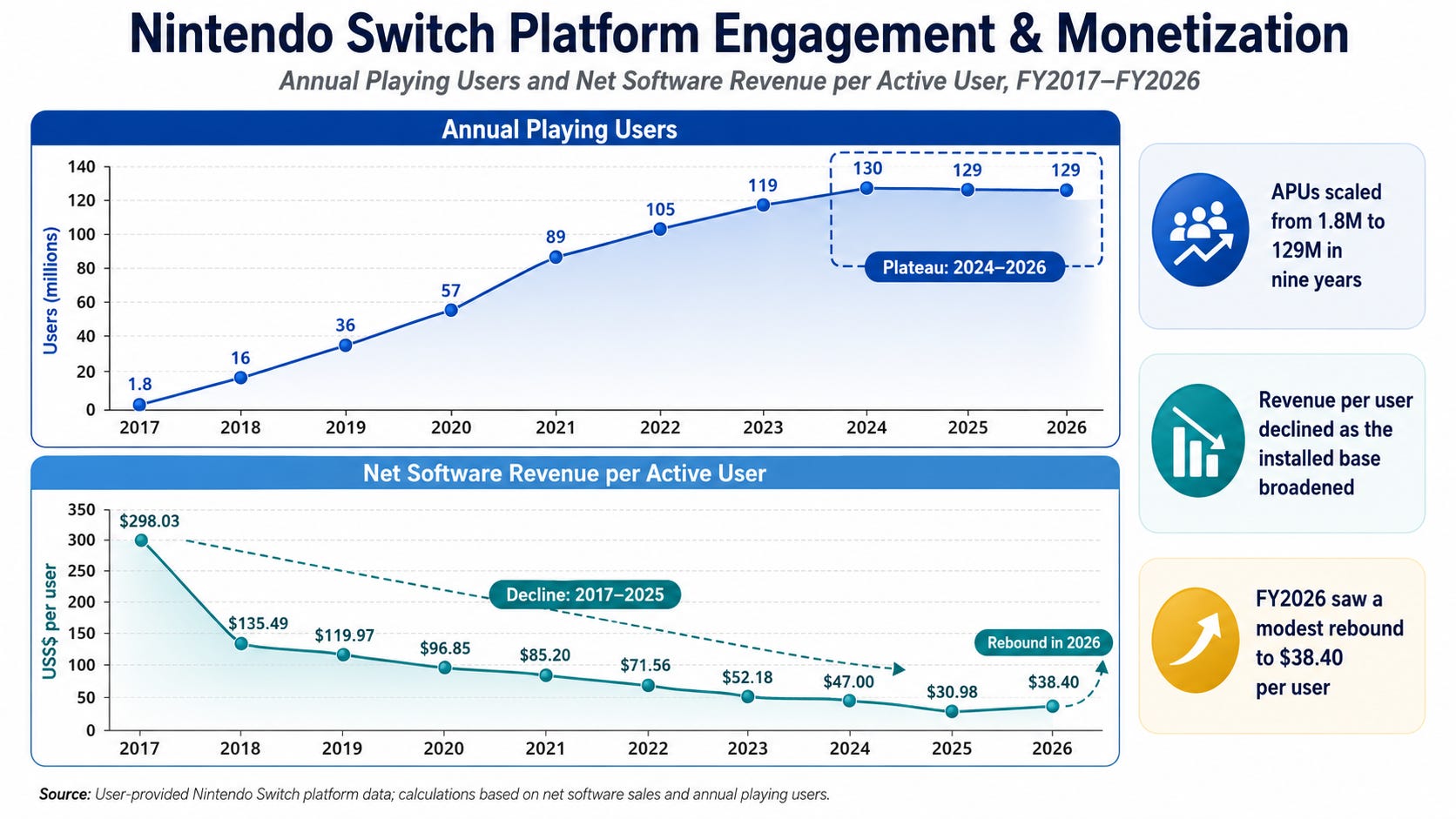

The most important Nintendo KPI’s are 1) the number of Annual Playing Users (APUs), and 2) net software revenue per APU. My view on valuation and the overall health of the business can be backed into these two numbers.

The numbers of APUs, which Nintendo defines as the number of users that have logged into their Switch account at least once in the last year, has flatlined since 2024. At face value this is concerning and describes the drought mentioned above that Nintendo is hoping to avoid with the Switch 2 via a more back loaded game release schedule. If the number of APUs were to start dropping, it would break the entire Switch ecosystem thesis. Obviously I don’t expect this to happen. In fact, holding APUs flat at the end of a 9-year hardware cycle amid weak new software releases is actually pretty impressive.

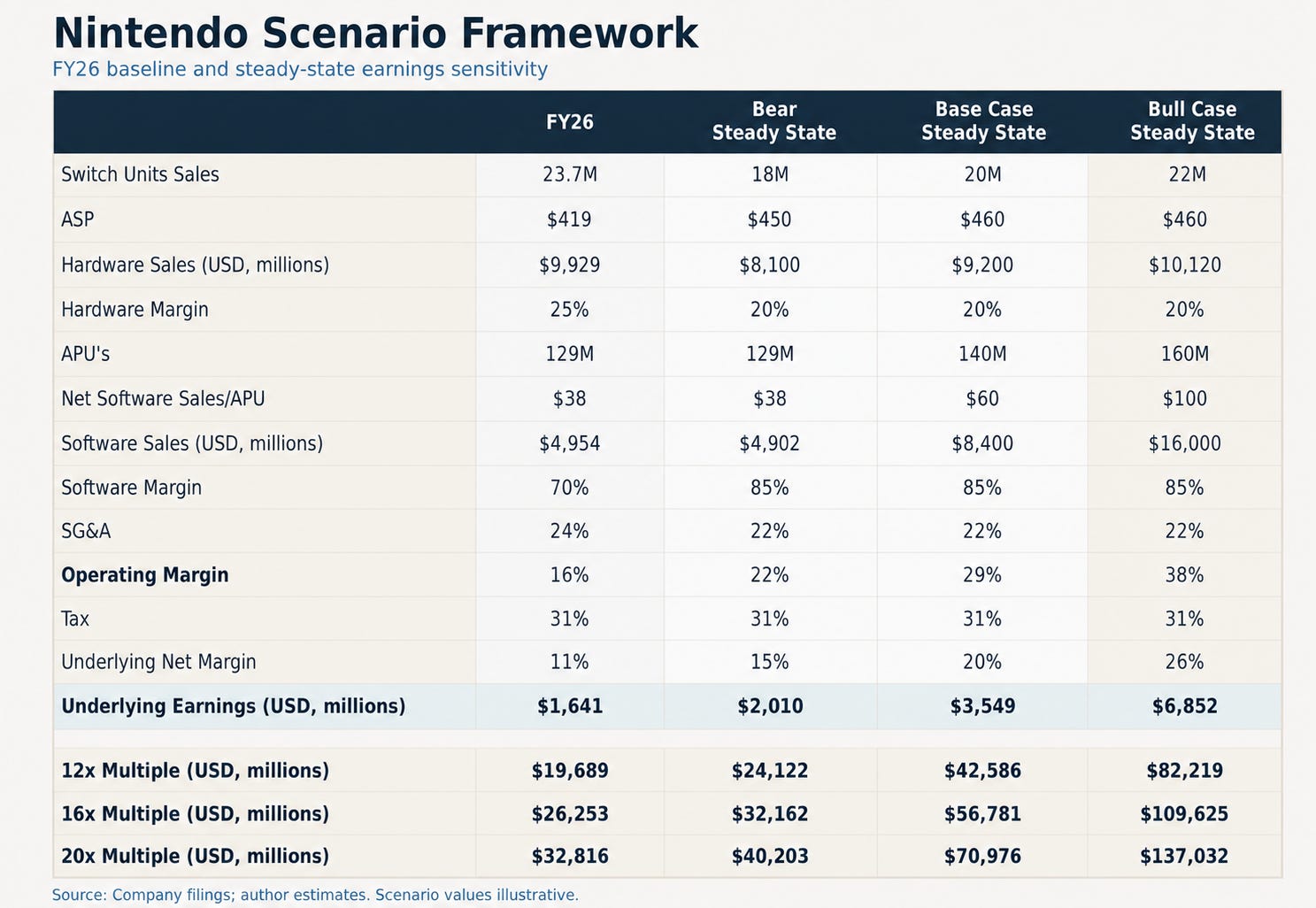

Normalized Switch unit sales of 18-20M per year seems about right as a conservative guess. This checks out when compared to the Switch’s average unit sales of 17M over its first 9 years, and also when considering the 5-7 year average device cycle. Normalized Switch unit sales should grow in line with APUs, hence its importance. I’m also assuming a gross margin of 20% on hardware, below the Switch 1’s ~30% margins from 2022 but above today’s temporarily pressured Switch 2 margins.

Net software revenue per APU has trended downwards since 2018, this number includes both video games sales and NSO subscriptions. This decline was to be expected because 1) The most hardcore Nintendo fans will buy Switch first and they have the highest revenue per user. As the less fanatic gamers join the Switch platform, they pull down the average software revenue per user. And 2) COVID saw a huge demand pull-forward which has now run off.

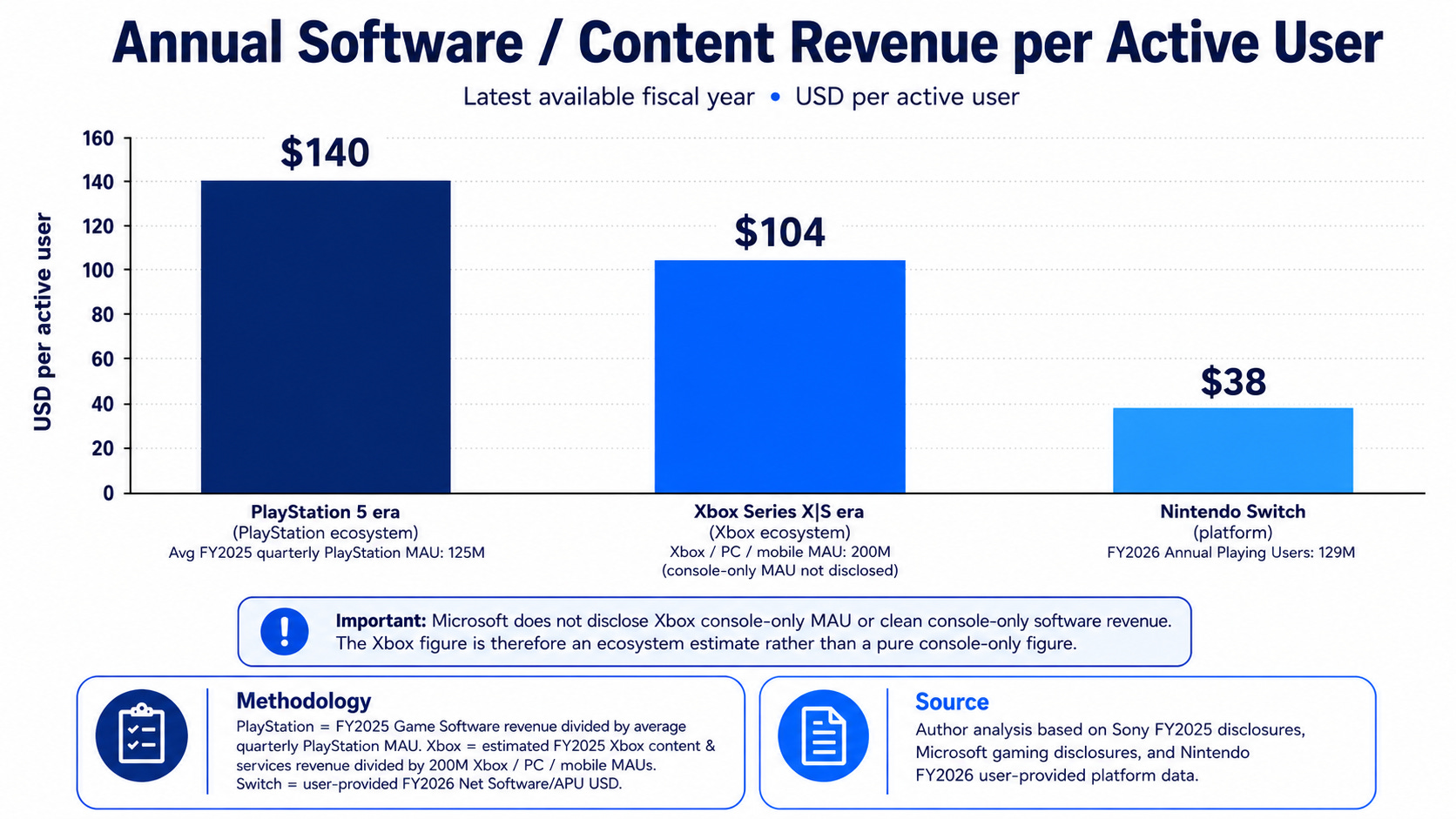

Going forward, net software revenue per APU should trend upwards. Despite the Switch being the more popular platform, it is well behind the Xbox and PlayStation when it comes to monetization. AAA games also come with higher average selling prices which given the influx of their availability on the Switch 2 will be a tailwind for net software sales. Nintendo Switch Online also has lots of untapped pricing power. The top NSO tier costs $49.99/year, unchanged since its original launch. Meanwhile the top tiers of PS4 and Xbox versions of NSO cost $159.99/year and $276/year respectively.

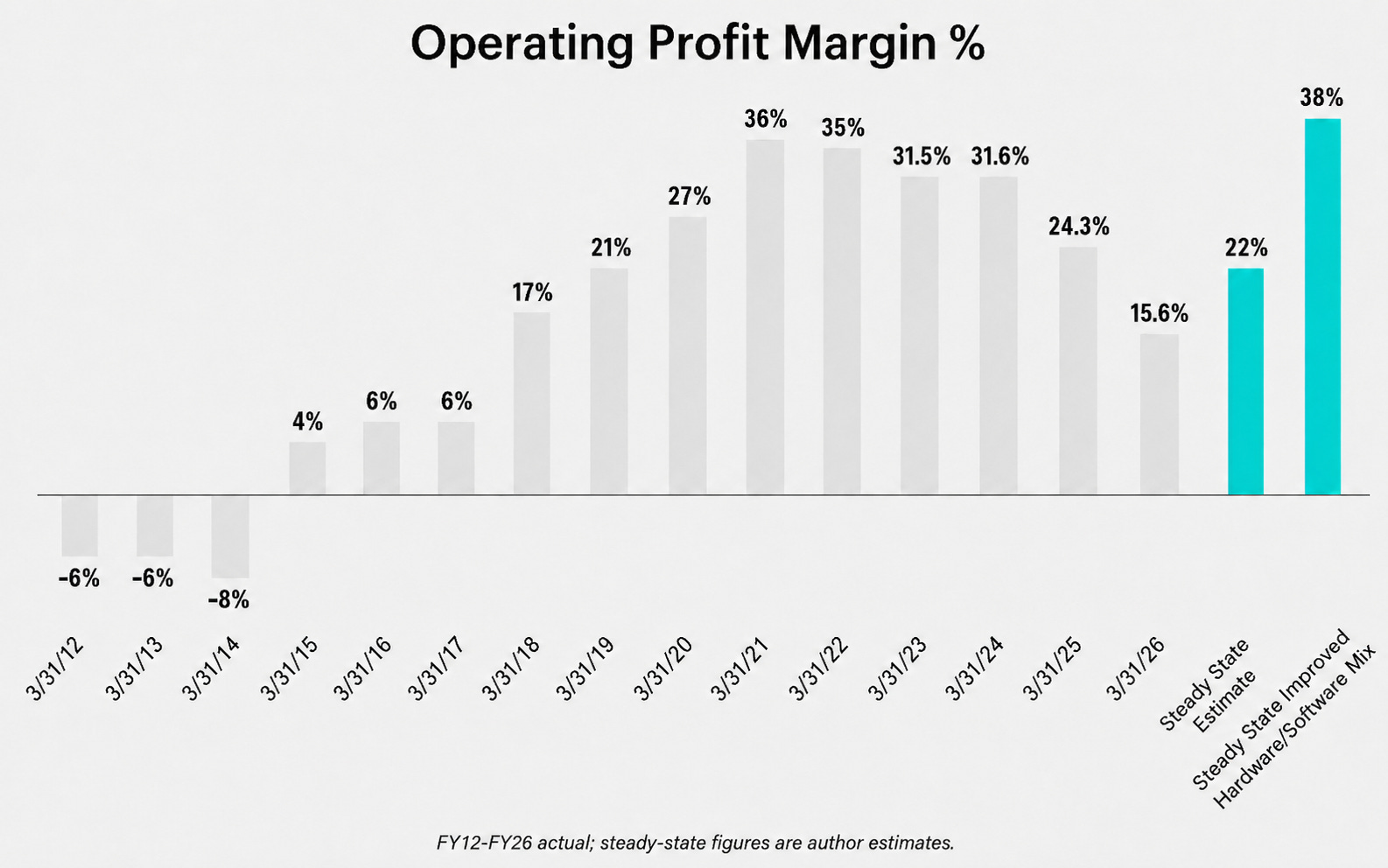

For longer-term software margins, I’m assuming 85% compared to ~70% today. This bakes in: 1) Digital sales expanding to 80% of total software sales vs 55% today and a mere 15% in 2017. There’s no cost to produce a physical copy and Nintendo gets the full retail instead of wholesale price so digital sales carry a ~90% gross margin instead of ~55% for physical. 2) Third-party gross sales rise to 60% of eShop sales vs ~50% today. Nintendo charges an estimated 30% take rate that carries near 100% gross margin. 3) Further expansion of high-margin NSO subscription and digital content sales.

R&D, marketing, and G&A should run around 22% of revenues. Again, these are conservative numbers. The corporate tax rate in Japan currently sits at 31%.

Putting this all together I get longer-term, “steady-state” hardware margins of 20% and software margins of 85%. At today’s hardware/software mix, which will only improve going forward, we arrive at an operating margin of 22%. We can then apply these steady-state margin assumptions to Nintendo’s current hardware and software revenues to get an idea of their underlying earnings power before applying an appropriate multiple.

The above steady state earnings estimates definitely err on the conservative side, and give zero credit to Nintendo’s growing IP business. I think we can also all agree that a 12x multiple is way too low for a business of this quality. In light of this, I don’t see how Nintendo’s core Switch Platform business could be worth anything below $25B. Realistically, I would assign a fair value upwards of $60B, and this still assumes essentially no APU growth and a below market multiple of 18x.

At today’s market cap of $54B, the downside is so protected it’s almost laughable. TPC and Nintendo’s other stakes are worth a conservative $27B. Add in their $14B of net cash and we are paying an implied $13B for the world’s best and most beloved game franchise along with the single greatest content creation track record of all time. Not to mention Nintendo’s swath of various other undisclosed assets, for example a portfolio of Kyoto real estate amassed over the previous century.

Don’t forget, that this business, for which we are buying for $13B, is in the early innings of its business transformation. My $60B valuation estimate assumes the Switch Platform largely plateaus at its current state. If instead Nintendo continues to execute, which all of the signs currently indicate, and APU growth resumes its trend upwards, there is a credible path to $110B+ in value.

Conclusion

Nintendo has released a staggering 21 of the 25 best-selling console and handheld games of all time. They are the undisputed video game console king and are backed by one of the most valuable media franchises on earth. Thanks to unwarranted short-term market fears, we have been offered a 2007 Apple-esque opportunity to buy into the IP fueled Switch ecosystem at a significant discount to its fair value. As this ecosystem continues to build momentum, investors will eventually wake up to the reality that Nintendo is no longer a low-margin hits-driven business, but instead a high-margin software fueled family of indefinitely-lived Switch devices.

I’m buying Nintendo today at ¥7,500/share, a 46% discount to my conservative fair value estimate of ¥14,000/share. If I’m wrong, and the Switch Platform initiative fails, my downside is more than protected by a large net cash position, TPC, and Nintendo’s various other hidden assets.

*Shares of Nintendo are also available via their ADR listing on the OTC Market.

Disclosure: This newsletter does not provide investment advice. Information presented is for informational purposes only and should not be considered a recommendation to buy or sell securities. The author may or may not own the securities discussed.